News and Business

FATF updates anti-money laundering and terrorism financing guide for real estate sector

International Financial Action Task Force (FATF) publication features mechanisms and best practices to fight money laundering and terrorism financing

As a sector involving high volumes of financial transactions, real estate is at increased risk of exposure to money laundering and terrorism financing (ML/TF). Accordingly, players in Brazil’s real estate sector are subject to various legal controls. They must also stay up-to-date with international recommendations and standards and base their internal procedures on the best market practices, reducing the risks involved in conducting real estate activities and adapting to the applicable legal obligations.

In Brazil, individuals and legal entities involved in real estate management, purchase or sale are required to comply with the rules of the Brazilian Money Laundering Prevention Law (Law No. 9,613/98) and observe Resolution No. 1,336/2014 of Brazil’s Federal Council of Property Brokers (COFECI). Real estate registry and notary offices also must comply with Provision No. 88/2019 of Brazil’s National Justice Council (CNJ).

The FATF and the AML/TF Real Estate Sector Guide

Established in 1989 by member countries of the Organization for Economic Co-operation and Development (OECD), the International Financial Action Task Force (FATF) is an intergovernmental organization for the prevention of money laundering and the financing of terrorism (AML/TF). In July 2022, it published an updated version of its AML/FT Guide for Real Estate Agents (Real Estate Sector Guide), originally published in 2008.

Seeking to increase good practices within the real estate sector, the guide outlines a risk-based approach (RBA) for individuals and public and private organizations. The guide is part of the FATF’s ongoing efforts to promote the RBA among Designated Non-Financial Businesses and Professions (DNFBPs) – a group including casinos, lawyers, notaries, independent accountants, trust and company service providers (TCSPs), real estate agents, dealers in precious metals and stones (DPMS), among others.

DNFBPs play a key role in protecting financial systems and global economies. They are also exposed to large amounts of information and many different economic players, which can increase their ML/TF risks. Accordingly, the FATF has provided numerous recommendations for the sectors in this group to mitigate these risks.

In this context, the Real Estate Sector Guide recommends implementing mechanisms and best practices for combating money laundering and terrorist financing based on analyzing each stakeholder’s specific risks. The publication also explains how to apply the recommendations the FATF prepared in 2012 for the real estate sector.

International perceptions of ML/TF risks

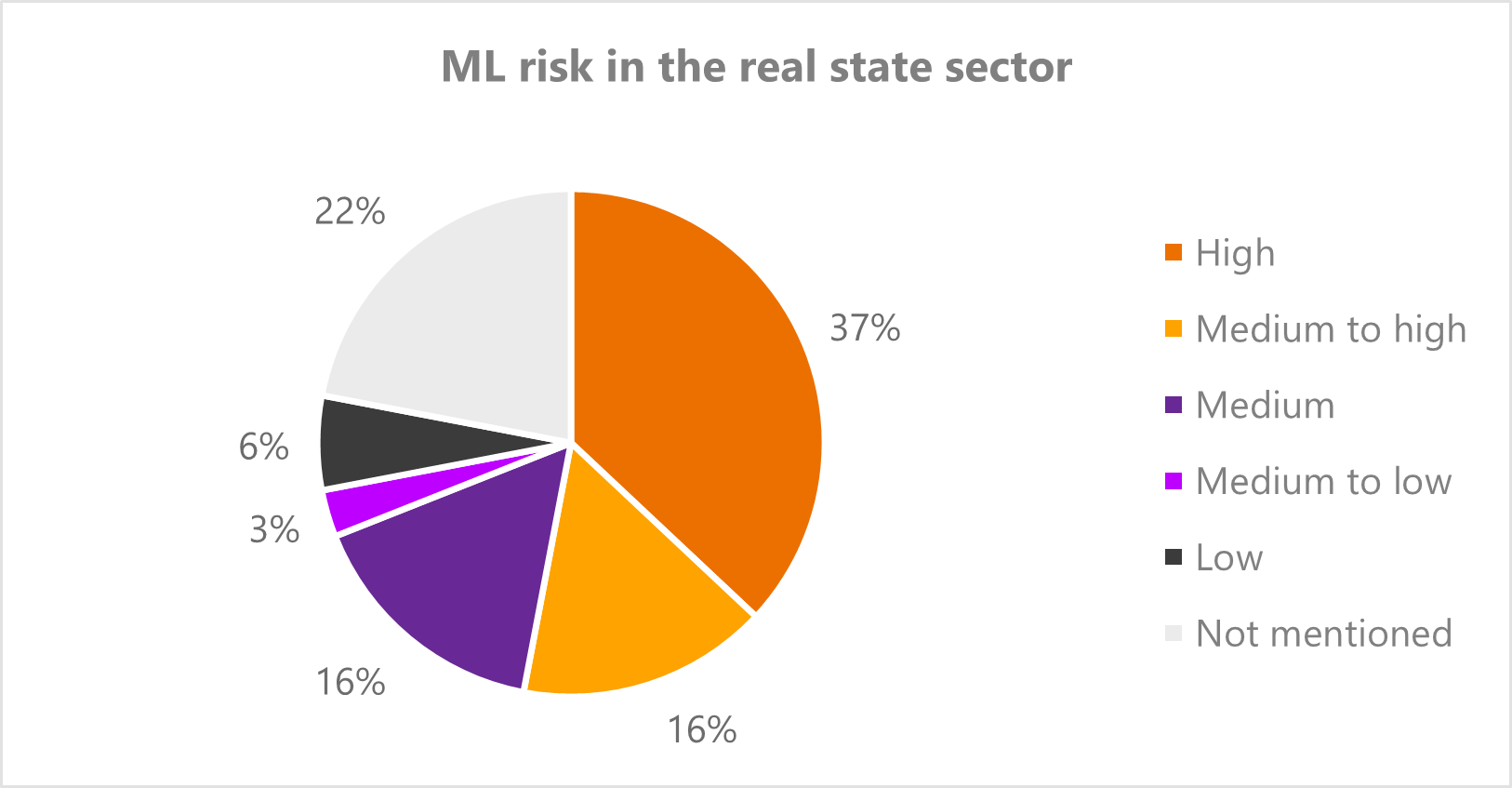

32 FATF-member countries and affiliated regional entities participated in the FATF’s 4th Round Ratings, providing information on their perception of money laundering and terrorism financing risks in the real estate sector. According to the results, 37% of participants believed the real estate sector presents a high ML risk (see the chart below, included in the Real Estate Sector Guide – item 31, p. 12):

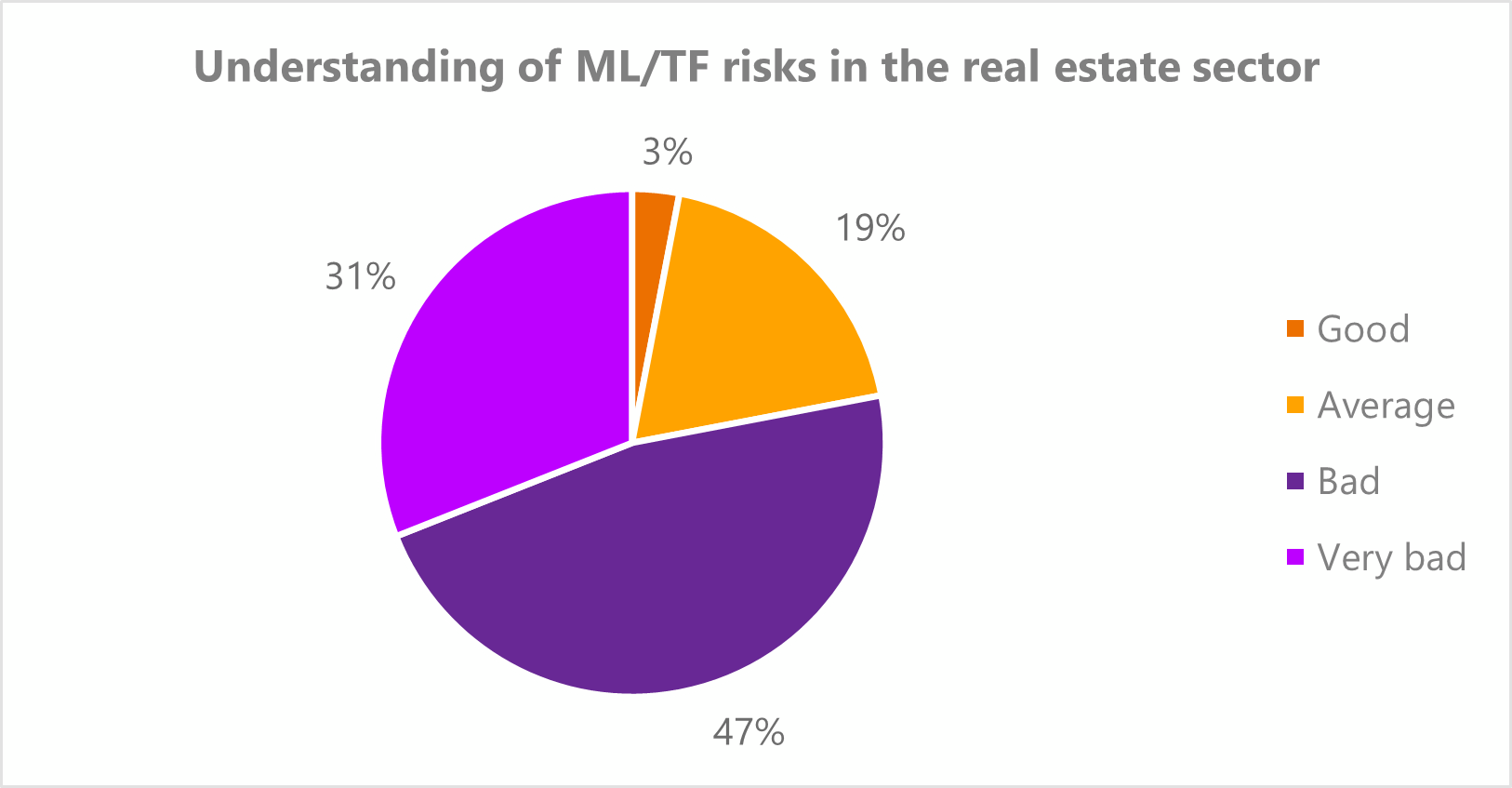

This survey also found that the participating countries’ respective real estate sectors have a low overall understanding of relevant ML/TF risks. As of 2021, 78% of the member countries in the 4th Round Ratings evaluated their real estate sector as either bad or very bad. The chart below shows this data (item 32, p.12):

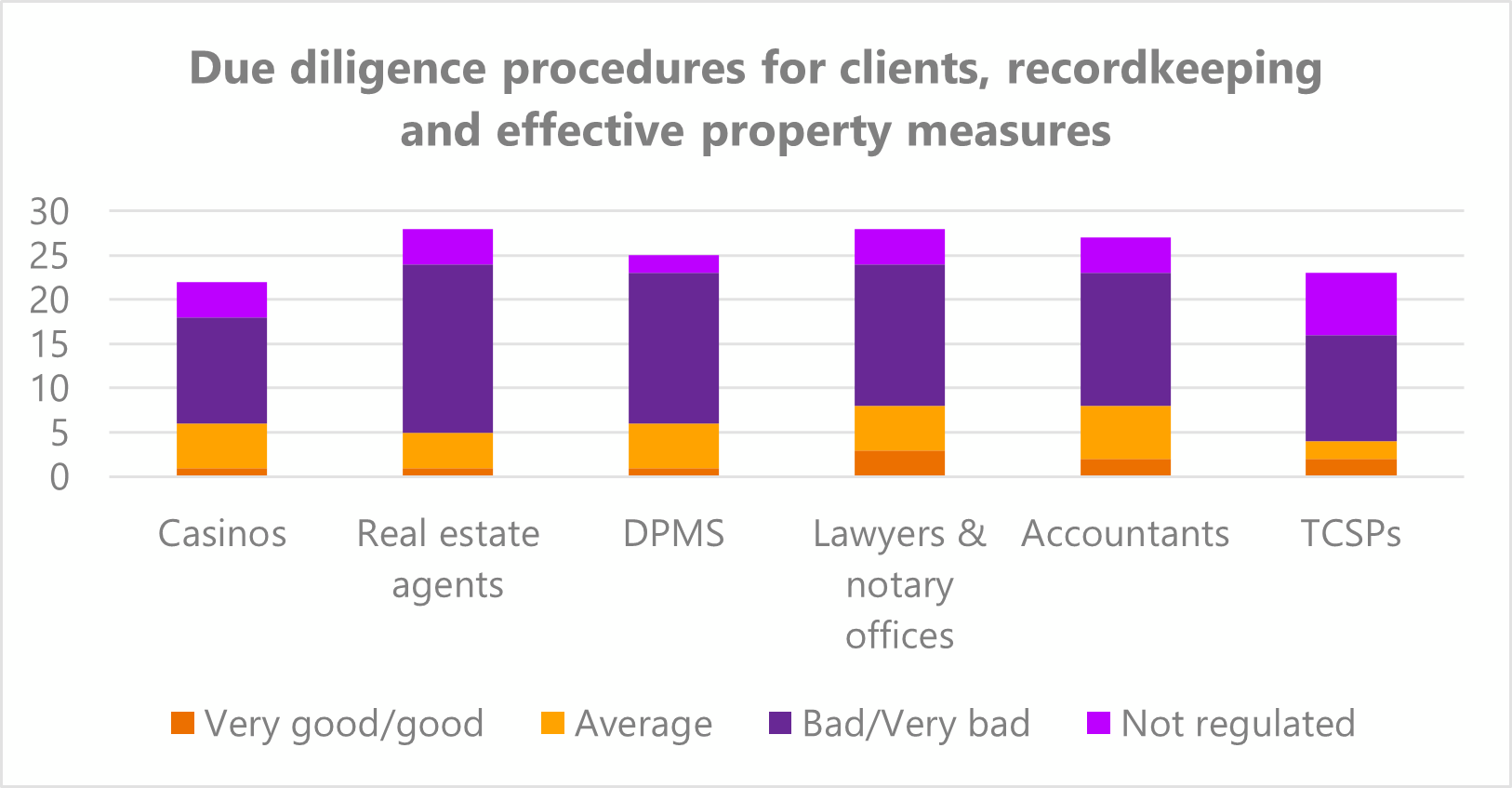

The 4th Round Ratings also revealed that only a minority of the countries considered the due diligence procedures for sellers and buyers in their respective real estate sectors (including recordkeeping and information requests regarding the final beneficiary) to be excellent or good. Moreover, the survey considered self-assessments of each type of DNFBP in regard to how well the respective procedures were implemented, as can be seen below:

The Real Estate Sector Guide makes it clear that real estate professionals in most of the assessed countries are not required to report suspicious transactions, despite obtaining large sums and conducting many transactions. This lack of regulation in the real estate sector makes it difficult to identify ML/TF risks.

Risk-based approach to ML/FT risks for the real estate sector

In implementing an effective RBA, the FATF recommends that players in the real estate sector – including builders, developers, real estate agents, lawyers, notaries, and any other professionals involved in the purchase and sale of real estate – should implement the following AML/TF controls:

Due diligence and risk analysis

Whether involved in purchasing or selling assets, real estate agents should conduct due diligence (item 22) and risk analysis (item 100) procedures to:

- Identify clients (buyers and sellers) and check for any hidden beneficiaries of the real estate transaction;

- Verify the nature of the transaction and the payment method used in the transaction (for example, the purchase and sale of residential or commercial real estate using cash or digital assets);

- Understand the purpose and nature of the professional relationship/transaction;

- Continuously monitor the progress of the relationship with clients;

- Check the origin and sources of client funds.

Criteria for a risk-based approach

Implement an RBA that considers and reflects:

- The legal and regulatory landscape;

- The nature, diversity and level of development of the different sectors required;

- The risk profile of the individual or legal entity;

- The risks regarding the geographic location of the real estate in the transaction;

- The size of the transaction;

- The financial value involved in the transactions;

- The risk of the clients involved (seller and buyer);

- The nature of the transaction (i.e., purchase and sale of residential or commercial real estate).

Additional measures

Adopt additional measures and more complete due diligence procedures for transactions concerning (item 115):

- Politically Exposed Persons (PEPs) may potentially divert and conceal public funds for personal enrichment (item 44);

- Real estate assets at prices far above or far below their market value, which may be a sign of illicit transactions (item 48);

- Foreign buyers, especially those from high-risk countries of origin – based on integrity indicators for the respective jurisdiction (item 49);

- Complex structures that make it difficult to identify the final beneficiary of the property – trust funds, for example (item 130);

- A failure to gather adequate information on the sources of the funds used for the transaction and a failure to check the accuracy or adequacy of buyers’ or sellers’ information (item 130);

- The involvement of buyers and sellers in suspicious transactions, whether paid in cash or virtual assets, without transparency and without clearly identifying the source(s) of payment (item 130).

Internal policies and controls

Implement policies and internal controls that effectively mitigate the risks identified, and maintain high internal investigation standards and procedures that guarantee qualified professionals work with AML/TF in the sector (items 62 and 140);

Compliance culture

Adopt and develop a culture of professional compliance within the real estate sector so that organizations can effectively address ML/TF issues (item 155);

Corporate governance

Companies in the sector should implement well-structured corporate governance programs to reduce their exposure to ML/TF, as well as compliance and reputational risks (item 141);

Responsibilities for risk analysis

Defining the roles and responsibilities of professionals working directly in the analysis of LD/FT risks, involving transactions and operations of real estate assets (items 144 and 154);

Training and awareness programs

Conduct training and awareness programs for professionals responsible for handling real estate transactions (items 63 and 162);

Regulatory obligations

Comply with all regulatory obligations (item 135 et seq.).

For further information, please contact Mattos Filho’s Compliance & Corporate Ethics, Real Estate and Forestry Investments practice areas.