News and Business

Merger control in Brazil: a 2024 retrospective and the outlook for 2025

An overview of the Brazilian Antitrust Authority's activities and expected trends in 2025

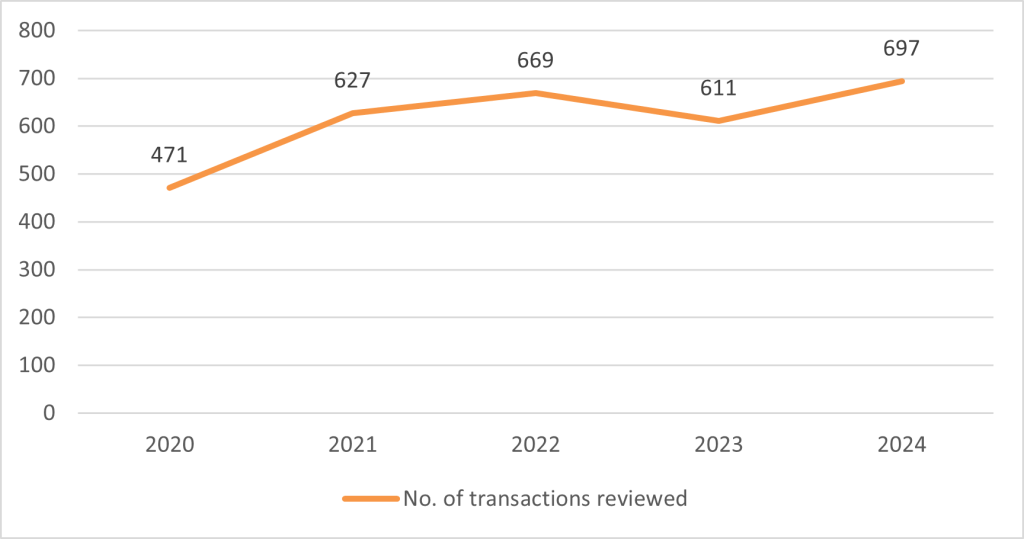

In 2024, CADE reviewed 697 merger cases – 644 (92%) via the fast-track proceeding and 53 (8%) via the regular proceeding, 11 of which were sent to CADE’s Tribunal for a final ruling. The total value of merger transactions reported in 2024 amounted to BRL 1.1 trillion (around USD 193 billion at current exchange rates). The average review period for cases submitted under the fast-track proceeding was 15.1 days (versus 12.6 days in 2023), while the average review period for cases submitted under the regular procedure was 93.9 days (versus 116.7 days in 2023), suggesting that CADE was able to increase its overall efficiency in reviewing merger cases.

The numbers indicate a rise in the number of mergers CADE reviewed, both when compared to 2023 (13%) and in relation to the last five years (a 47% increase in comparison to 2020).

Reviewed merger transactions, 2020-2024

Significant cases and expected trends in 2025

2024 was marked by important decisions at CADE’s Tribunal regarding the methodology for calculating gun jumping fines, with the Tribunal indicating it would apply a cap of 20% of the transaction value in such cases. This approach was initially used in the context of an investigation into Kurumá’s acquisition of tangible and intangible assets from Govesa (APAC No. 08700.005463/2019-09) before subsequently being used in two other cases (APAC No. 08700.003447/2020-15 and No. 08700.009227/2022-59).

In these cases, CADE’s Tribunal indicated that there could be situations where this 20% cap may not apply, such as:

- If the parties acted in bad faith;

- If the value of the transaction is merely symbolic; or

- Transactions that may pose significant competition-related concerns.

Another key development in 2024 concerned how CADE determines whether certain transactions are subject to review.

In the first half of the year, CADE’s Tribunal issued an important decision in a gun jumping investigation into Digesto and JusBrasil (APAC No. 08700.000641/2023-83), which involved an extensive debate about the definition of ‘economic group’ for the purpose of calculating revenues.

Based on the reporting commissioner’s vote, the Tribunal clarified that a shareholder holding 20% or more of the equity interest in the party directly involved in the transaction is not presumed to have control over it merely for this reason. In this regard, CADE would have to determine control via a concrete analysis of the shareholder’s governance rights. Moreover, the reporting commissioner listed certain rights that CADE’s General Superintendence (GS) has historically considered as indicative of control, which, at a minimum, provides suggestions of parameters that may be considered in future cases. However, the Tribunal’s decision did highlight that CADE still needs to discuss this subject in-depth to provide clearer standards and more legal certainty.

In 2024, the GS issued several decisions concerning the need to report real estate acquisitions. In two cases involving non-operational properties from the Carrefour Group (Merger Case No. 08700.001216/2024-92 and Merger Case No. 08700.000735/2024-33), the GS concluded that these transactions did not represent ‘concentrations’ as defined in the Brazilian Competition Law. This was mainly based on the fact that the properties (in their current state) would not increase the buyer’s production capacity, considering both the buyer’s activities and the need for investments to make the properties operational. However, the GS issued a contrasting ruling in a subsequent case also involving the Carrefour Group (Merger Case no. 08700.002034/2024-39). In the GS’s view, as the acquisition of the property was being made by a company operating in the real estate sector, this meant the property itself was an essential asset.

In light of these rulings, Bompreço Bahia submitted a formal consultation to CADE’s Tribunal (Consultation No. 08700.007814/2024-75), questioning whether a sale of a non-operational property should be considered a reportable transaction. CADE’s Tribunal reviewed the case on February 14, 2025, during which the reporting commissioner noted that the distinction between ‘property’ and ‘commercial establishment’ was essential in analyzing the case. According to the commissioner, a commercial establishment encompasses a set of already organized assets that allow for carrying out an economic activity. In this regard, he concluded that the mere acquisition of a non-operational property does not constitute a reportable transaction, as it does not involve a productive asset.

However, the reporting commissioner did distinguish certain cases that could be considered reportable transactions, such as those involving:

- The transfer of properties that are operational at the moment when commercial negotiations begin between the parties;

- Situations where the property transfer is part of a broader transaction involving other assets that constitute a commercial establishment; and

- The transfer of properties considered essential assets for regulatory reasons.

He also noted the need for case-by-case evaluations in the event of transactions between companies active in the real estate sector (such as construction developers).

The practical application of these consolidated criteria should establish an important trend in 2025, as the real estate sector is one of the most active in terms of filing merger transactions with CADE.

During 2024, the GS’s move to proactively investigate non-reported transactions involving technology companies – and, particularly, artificial intelligence – marked another significant trend. The GS initiated an ex officio preliminary investigation to confirm whether the following deals would be reportable in Brazil:

- A partnership between Anthropic and Amazon (APAC No. 08700.005962/2024-55);

- A partnership between Mistral AI and Microsoft (APAC No. 08700.005961/2024-19);

- An agreement between Character.ai and Google (APAC No. 08700.005638/2024-37).

The first two transactions are also subject to the scrutiny of other competition authorities, particularly the UK’s Competition and Markets Authority. The investigations are still ongoing but are indicative of CADE’s interest in technology-related transactions, even when they take place outside Brazil.

The above cases reinforce the need for companies to carefully assess in advance whether their transactions – including mergers and acquisitions, as well as partnerships and real estate acquisitions – should be filed with CADE.

Finally, in 2024 the first merger transactions were filed via CADE’s e-Notifica system, launched at the end of 2023 (as reported in previous editions of this bulletin). The system established an electronic process for reporting transactions eligible for the fast-track proceeding, the system is integrated with other public databases in Brazil to assist the authority in reviewing such cases with greater speed and efficiency. In response to feedback from companies that submitted transactions, in November 2024, CADE launched an updated version of the system. The GS has already announced that in the future, it intends for all fast-track transactions to be reported via this system.

For more information on these topics, please contact Mattos Filho’s Antitrust practice area.