News and Business

IP contracts in Brazil: simplification of the INPI’s requirements and new tax rules

Among the highlights are the Brazilian Industrial Property Office (INPI)'s new understanding on the license of non-patented technology and the impacts of MP 1,152/2022 on the payment of royalties

At the end of 2022, Brazil implemented two important changes that significantly impacted the field of intellectual property, especially in regard to contracts. First, the INPI issued new regulations to enable the licensing of non-patented technology and considerably simplify procedures for registering and recording technology transfer contracts. Second, Provisional Measure No. 1,152/2022 was also enacted to establish new transfer pricing rules, which apply to royalties.

New INPI provisions

As provided for in Brazil’s Intellectual Property Law (Law No. 9,279/1996 – LPI), contracts concerning the licensing or assigning of industrial property rights must either be annotated (for patents, trademarks, industrial designs) or registered (for technology supply, franchise, technical and scientific assistance services) with the INPI to be effective and enforceable vis-à-vis third parties. The INPI considers such contractual instruments as technology transfer contracts.

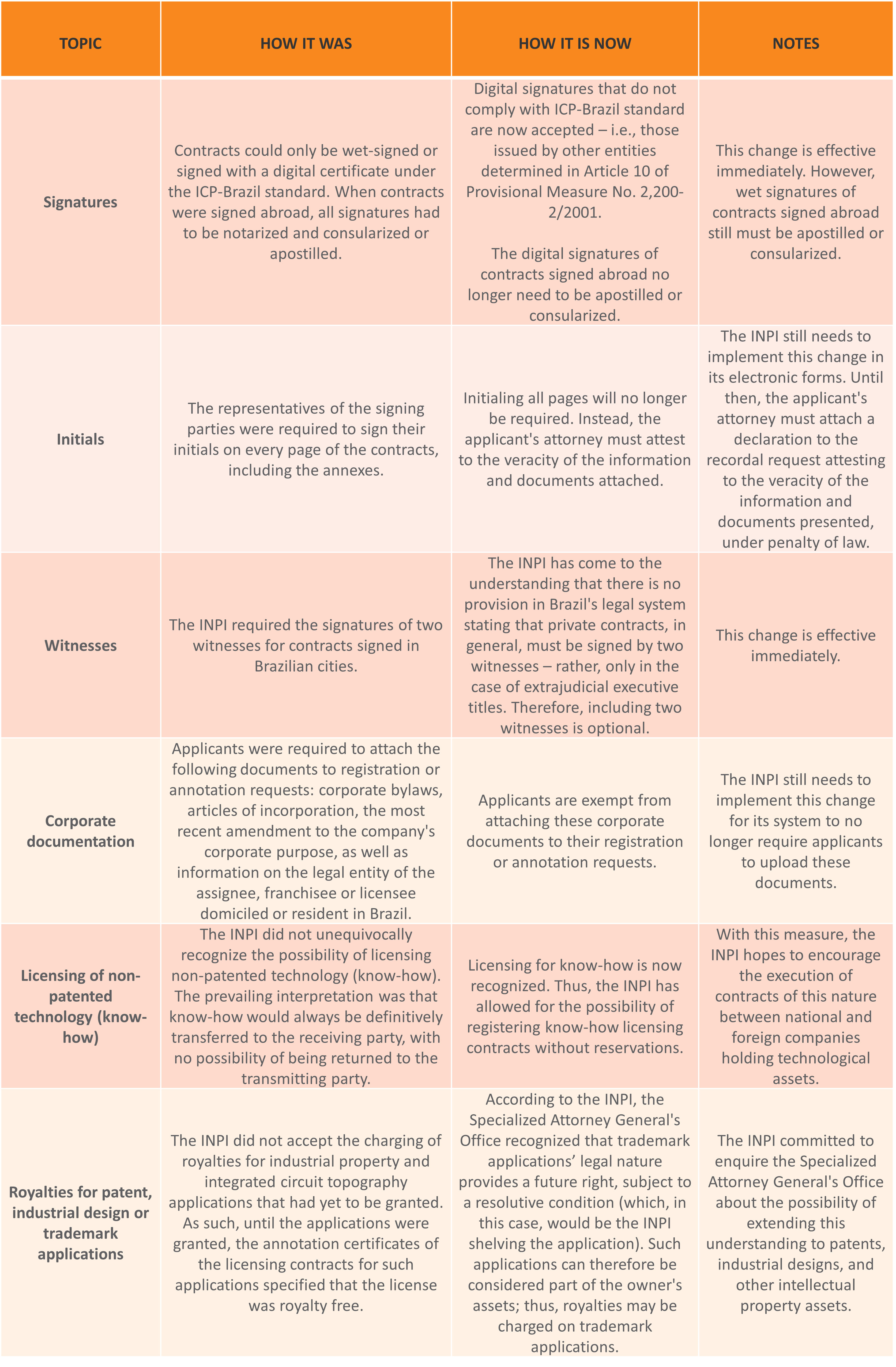

Historically, the analysis and recordal of these instruments were conditioned to the fulfillment of a series of requirements from the INPI, as well as restrictions on certain types of transactions or provisions. Notably, the INPI understood that it was not possible to register licenses for non-patented technology.

The changes to the INPI’s position and procedures are featured in Edition No. 2,713 of its Industrial Property Journal (Revista de Propriedade Intelectual). These developments ensure greater legal certainty and streamlined processes for formalizing intellectual property contracts.

The main changes are outlined below:

Furthermore, in the wake of previous positions formalized through Normative Instruction INPI/PR No. 70/2017 and Resolution INPI/PR No. 199/2017, the INPI has reiterated that it does not have the jurisdiction to determine payment limits regarding the remittance of royalties abroad between related companies. The office also stressed it would not take a stand on the value and terms for fiscal and economic aspects of intellectual property contracts, unless ordered to do so by the competent bodies.

In giving private agents increased autonomy, these changes are expected to strengthen Brazil’s institutional environment and create incentives for economic development.

Tax aspects

In the tax field, the recently enacted Provisional Measure No. 1,152/2022 has changed how Corporate Income Tax (IRPJ) and Social Contributions on Net Profit (CSLL) are levied on transfer pricing transactions. This has impacted the Brazilian tax system in many ways, including directly affecting the deductibility of royalty payments.

The key changes involve:

- Express provisions for transactions involving intangible assets, including those that are difficult to valuate;

- Rules for determining the calculation basis for the provision of intra-group services, which, within the scope of intellectual property, may include technical and scientific assistance services;

- Provisions for drawing up cost-sharing contracts (including cooperation and technological partnership contracts) and establishing how participants will make their contributions;

- Repealing provisions in Law No. 4,131/1962, Law No. 4,506/1964, and Decree-Law No. 1,730/1979 that limit both the percentages of net revenue from sales of manufactured products and the situations where the payment of royalties is tax deductible (for example, royalties paid to company partners are currently not deductible);

- Repealing both Article 50 of Law No. 8,383/1991 (and its amendments, as implemented by Law No. 14,286/2021) and Article 12 of Law No. 4,131/1962, which established the obligation to register and annotate contracts with the INPI for tax deduction purposes;

- When determining the actual profit and CSLL calculation basis, any financial values paid, credited, delivered, used or remitted either as royalties or for technical, scientific, administrative or similar assistance are non-deductible if due to beneficiaries in tax havens or jurisdictions with favored taxation status and privileged fiscal regimes. This is also the case for related parties when deducting such values results in double non-taxation.

Although these changes become effective as of January 1, 2024, taxpayers may elect to apply them (irrevocably) to the 2023 calendar year. The Brazilian Federal Revenue (RFB) will define the method, deadline, and conditions for taking up this option.

In any case, the Brazilian Congress should convert Provisional Measure No. 1,152/2022 into law within 120 days (the month of January does not count toward this deadline, as Congress is in recess). If it is not converted into law, Congress must issue a legislative decree in order to regulate its legal effects.

As such, Provisional Measure No. 1,152/2022 introduces interesting changes to certain contracts. For example, it will allow companies to increase the percentage of royalties they remit abroad, as these will be deductible. However, when checking if it is worth already adopting the changes for 2023, companies should assess the scope of the provisional measure’s application and its potential impact on their operations.

The changes reported above are aligned with general efforts to modernize and reduce bureaucracy, which have especially been promoted by regulatory changes implemented by the Economic Freedom Law (Law No. 13,874/2019) – which sought to reduce state intervention in the exercise of economic activities – and by Brazil’s recent Foreign Exchange Reform (Law No. 14,286/2021), which took effect on December 31, 2022.

For further information, please contact Mattos Filho’s Intellectual Property and Tax practice areas.